March 2026 was a month, Indian equity investors would

rather forget. Both the Sensex and Nifty 50 ended deep in

the red, battered by a toxic cocktail of geopolitical shock,

surging crude oil prices, and relentless foreign selling.

What began as a volatile but seemingly manageable

correction quickly snowballed into one of the most

punishing months for Indian benchmarks in recent

memory, erasing months of gains and wiping out an

estimated ₹48 lakh crore of investor wealth in a matter of

weeks.

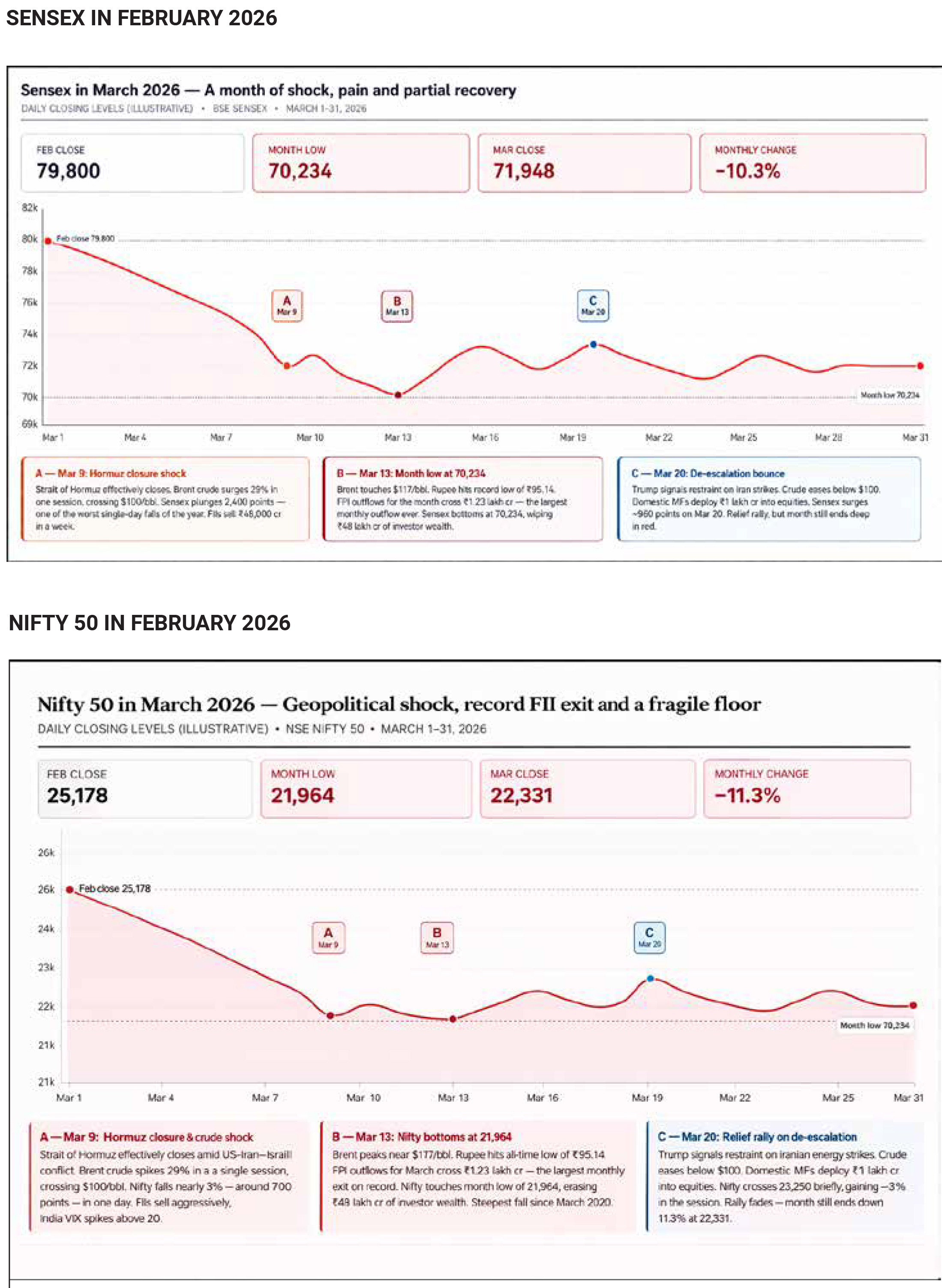

The Nifty 50 closed March at approximately 22,331 — a

fall of roughly 2.9% from its February end level of around

25,178. The Sensex fared even worse, shedding over 10%

across the month to close near 71,948, down sharply

from its late-February levels. March was punctuated by

repeated gap-down opens, savage intraday swings, and

brief but ultimately hollow relief rallies that lured buyers

in, only to reverse and fade. The India VIX, the market's

fear gauge, spiked above 20 for extended periods — a

clear signal that institutional players were paying heavily

for downside protection, and that genuine confidence

had left the room.

The cause of March's mayhem was a sharp escalation of

geopolitical tensions in West Asia. Conflict involving

Iran-linked flashpoints — which had been simmering

through February — intensified dramatically around the

last few days of that month, triggering a classic risk-off

cascade across global markets. For India, the damage

was immediate and multi-channelled. The most direct hit

came through crude oil. Brent crude surged above $100

per barrel in the first two weeks of March — a

psychologically significant threshold that set alarm bells

ringing for India, the world's third-largest oil importer.

Every dollar increase in crude adds meaningfully to

India's import bill, widens the current account deficit,

pressures the rupee, and stokes inflation. Markets

moved quickly to price in all these consequences. The

Nifty fell nearly 3% in a single session on 9 March, with

the Sensex shedding over 2,400 points in one of the

sharpest single-day drops in recent months.

If geopolitics lit the fire, Foreign Institutional Investor

selling poured fuel on it. FIIs turned aggressive net

sellers in March, with net outflows estimated at

₹14,000–₹48,000 crore over the course of the conflict's

escalation. The logic was straightforward: when

geopolitical risk spikes, global funds rotate out of

emerging market equities — perceived as higher-risk

assets — and into safe havens like US treasuries, gold,

and the dollar. India, despite its relatively strong

domestic macroeconomic fundamentals, was caught

squarely in this global de-risking wave.

The rupee came under simultaneous pressure, sliding to

fresh lows against the dollar. A weaker rupee

compounds the crude oil pain further — India pays for its

oil imports in dollars, so every rupee of depreciation

makes an already expensive barrel of oil even costlier in

local currency terms. This feedback loop between crude,

the rupee, and inflation fears kept sentiment firmly

negative throughout most of the month.

The pain was not evenly distributed across the market. The sectors that bore the heaviest losses were those most exposed to the dual threat of higher crude and tighter financial conditions — banks and NBFCs, automobile companies, aviation stocks, paint manufacturers, and logistics firms. These sectors together carry significant weight in both the Sensex and Nifty, which amplified the benchmark-level damage. There were pockets of resilience. Upstream oil and gas producers benefited from higher crude realizations and select IT and pharmaceutical names attracted some safe-haven interest on the back of rupee depreciation, which boosts export earnings. However, these sectors are relatively underweight in the large-cap indices compared to financials and consumer-facing businesses, so their gains were insufficient to offset the broader carnage. Interestingly, mid-cap and small-cap indices showed slightly better relative performance during parts of the month — but even these couldn't escape the overall negative tide. The month wasn't entirely without hope. In the latter half of March, comments from US President Donald Trump hinting at a more restrained approach toward Iranian energy infrastructure — effectively signalling a pause in the threat of direct military strikes — triggered sharp short-covering rallies. On 20 March, the Sensex surged nearly 960 points and the Nifty briefly crossed 23,250 as crude eased and risk appetite ticked up globally. Global equity funds recorded their largest weekly inflow in over two and a half months in the week ending 25 March, as markets reacted positively to the de-escalation signals. FII outflows from India slowed noticeably in this window, and some short covering in index heavyweights provided temporary support. But the key word is temporary. Each time Trump's tone softened, markets rallied. Each time his rhetoric hardened again — as it did in early April with fresh threats — the selling pressure returned. The de-escalation comments acted more as a brake on panic than as a genuine catalyst for a structural reversal. By month end, FII flows remained in net negative territory. March 2026 has been a sobering reminder of how quickly external shocks can overwhelm strong domestic fundamentals. India's GST collections, formal sector activity, and credit growth all remained reasonably healthy through the month — but these factors were simply no match for the combination of a $100 crude shock, record FII outflows, and a global flight to safety.

March 2026 was a difficult month for Indian debt

markets, with higher yields and softer prices across most

segments as a confluence of external shocks and

domestic structural pressures overwhelmed the RBI's

earlier liquidity support measures. From government

securities to corporate bonds, the broad message from

the fixed income market was consistent: the cost of

borrowing was moving up, and the rate cut narrative that

had animated markets earlier in the fiscal year was

losing conviction fast.

The benchmark 10-year government securities yield told

the clearest story, rising to approximately 7.00% by 30

March 2026 — up roughly 32 basis points over the month

and about 42 basis points higher than a year ago. This

was a meaningful move, reflecting a genuine repricing of

inflation risk and term premiums rather than a technical

blip. Shorter-dated instruments were relatively more

insulated, with RBI's liquidity operations helping cap the

worst of the selling at the short end, but longer-duration

bonds took the brunt of the pressure. State Development

Loans tracked the G-Sec move closely, with yields in the

6.6–7.8% band across the 3 to 30-year maturity

spectrum, and spreads over central government bonds

widening

as

investors demanded

additional

compensation for fiscal and geopolitical uncertainty at

the state level.

The dominant external driver was, of course, the West

Asia conflict and its most immediate market

consequence — Brent crude crossing $100 per barrel. For

India, a country that imports roughly 85% of its crude oil

requirements, a three-digit oil price is not just an energy

story; it is simultaneously an inflation story, a current

account story, and a currency story. Markets moved

quickly to price in all three dimensions. Higher crude

threatened to push CPI inflation — already nudging up to

around 3.2% in February 2026 from earlier lows — further

toward the upper bound of the RBI's comfort zone. This

effectively closed the window on meaningful near-term

rate cuts that bond markets had been partially pricing in,

forcing a broad yield curve adjustment, particularly

beyond the 3 to 5-year segment where rate cut

expectations had been most aggressively embedded.

Domestically, the debt market was grappling with a

supply problem that predated the geopolitical shock. The

central government had announced gross G-Sec

borrowing of ₹17.2 lakh crore for FY2027 — above

market expectations — and states had front-loaded their

own borrowing calendars aggressively in the January to

March quarter, adding approximately ₹5 trillion of net

supply. This volume of paper hitting the market

simultaneously kept yields structurally elevated,

regardless of RBI's compensating measures. The fiscal

deficit for FY2025-26 was revised to approximately 4.5%

of GDP, marginally above the original 4.4% target, and the

central government's debt-to-GDP ratio was estimated to

have risen to around 57% for FY26 — numbers that

reinforced the market's view that India would need to

issue substantial fresh debt for several years to come,

keeping term premiums firm at the long end.

The RBI was not passive. It had already injected

significant liquidity through LTROs, open market

operations, and repo channel easing in the preceding

months, and continued to provide support via buying in

the "Others" category during March. This helped prevent

a disorderly spike, particularly at the short end — T-bill

yields cleared in the 5.3–5.6% range, while OIS and

MIBOR-linked rates remained well below their peak

liquidity-tight phase levels. However, the incremental

demand generated by RBI operations was simply

insufficient to offset the heavy supply pressure and the

repricing of long-end risk, leaving the yield curve biased

higher on balance.

In the corporate bond space, March saw the highest

issuance volumes in eleven months, with around ₹990

billion raised — a sign that corporates rushed to lock in

funding ahead of fiscal year-end. But the pricing told a

less comfortable story: spreads over G-Secs widened to

above 80 basis points from an earlier 50–60 basis point

range, as risk premiums for credit expanded in line with

the geopolitical and inflation backdrop. Major public

sector banks including SBI, Bank of Baroda, Indian Bank,

and Union Bank issued 7 to 10-year paper at yields in the

7.1–7.2% band — meaningfully higher than equivalent

issuances earlier in the fiscal year.

For debt mutual fund investors, the month delivered a

sobering reality check. Longer-duration G-Sec funds

reported flat to negative returns as underlying bond

prices fell in tandem with rising yields. Short-duration

and liquid fund investors fared better, sheltered by RBI's

short-end support and the relative stability of T-bill rates.

There was some rotation out of equity products — hit

hard by the West Asia-driven equity market sell-off — into

high-quality investment-grade debt, but this incremental

demand was not enough to reverse the prevailing

yield-up trend.

March 2026 proved to be a frustrating month for bullion

investors in India — plenty of drama, but ultimately little

reward. Both gold and silver ended the month lower than

where they started, despite a geopolitical backdrop that, in

theory, should have been tailor-made for safe-haven assets.

The West Asia conflict delivered sharp spikes and

gut-wrenching reversals in equal measure, leaving the

month characterised less by a clear directional trend and

more by exhausting whipsaw volatility that tested the nerves

of traders and long-term holders alike.

Gold in the domestic market started March around ₹14,309

per gram before sliding to a net lower close by month end,

with intraday swings of several hundred rupees per 10

grams becoming a near-daily occurrence. The month's most

dramatic session came on 26 March, when gold surged over

₹3,000–3,700 per 10 grams in a single day on the back of

global risk-off sentiment and a briefly softer dollar — but this

move came after the metal had already given up far more

ground earlier in the month. Silver's journey was even more

turbulent. Starting near ₹2.95 lakh per kilogram, silver briefly

touched ₹3.15 lakh in early March before collapsing to

approximately ₹2.5 lakh by month end — a decline of roughly

5% that significantly outpaced gold's losses, reflecting

silver's greater sensitivity to both industrial demand

conditions and speculative positioning.

The story of why bullion underperformed despite an active

regional conflict comes down to one dominant factor: crude

oil and its knock-on effects on interest rate expectations.

When US-Israel strikes on Iranian targets triggered the initial

escalation in late February and early March, gold and silver

responded exactly as textbook safe-haven logic would

predict — MCX gold briefly surged above ₹1.66 lakh per 10

grams while silver touched multi-month highs. But the same

conflict that drove investors into gold also drove Brent crude

above $100–110 per barrel, and that oil spike carried a sting

in its tail. Higher crude meant higher global inflation, which

in turn pushed back expectations of rate cuts from the US

Federal Reserve and other major central banks. Since gold

and silver are non-yielding assets, rising real rate

expectations make them structurally less attractive, and the

market wasted little time in repricing that reality. By

mid-March, gold had shed ₹12,000–20,000 per 10 grams

from its early-month peak, and silver had corrected by

₹30,000–1 lakh per kilogram — steep reversals that unfolded

even as the underlying geopolitical conflict showed no signs

of resolution.

The dollar and US Treasury yields added further

headwinds. While geopolitical uncertainty initially

softened the dollar and lent some support to bullion, the

subsequent shift toward a more hawkish rate narrative

strengthened the greenback and pushed up Treasury

yields — a combination that typically pressures

dollar-denominated gold and silver prices, with the effect

transmitted directly into Indian rupee-denominated

domestic rates.

A late-month bounce on de-escalation talk — gold up

roughly 1% and silver jumping nearly 4% on MCX in the

final sessions — offered some consolation but did not

meaningfully alter the month's outcome. March 2026

ultimately delivered the worst of both worlds for bullion:

maximum volatility with negative returns, as the

rate-hawkish oil shock proved a more powerful force than

the war-risk safe-haven premium.

March 2026 will be remembered as a historic and deeply

uncomfortable month for the Indian rupee. The currency

breached the psychologically significant ₹93 per US

dollar mark for the first time ever around 20 March, went

on to touch an intraday record low of approximately

₹95.14, and eventually settled around ₹93.50 by month

end — implying a monthly depreciation of roughly 2–3%

and a cumulative 12-month slide of nearly 9–10% from

the ₹84–85 levels that prevailed in mid-2025. In absolute

terms, this was one of the steepest single-month

depreciations the rupee has ever recorded.

The primary culprit was the West Asia conflict and its

most immediate consequence for India — a crude oil

price shock. Brent crude surged to $110–117 per barrel,

far above the RBI's assumed baseline of around $70,

dramatically expanding India's dollar-denominated oil

import bill. Since India sources roughly 80% of its crude

requirements from overseas and pays in dollars, the

spike translated directly into surging dollar demand in the

domestic foreign exchange market, putting relentless

downward pressure on the rupee. Compounding this was

the behaviour of Foreign Institutional Investors, who

turned aggressive net sellers of Indian equities through

the month, repatriating an estimated $8–10 billion out of

the country and generating a sustained second wave of

dollar demand that the market struggled to absorb.

The global backdrop offered no relief. The US dollar index

traded near multi-month highs around 99–100, as the

Federal Reserve's higher-for-longer rate narrative drew

capital into dollar assets and away from emerging market

currencies. In this environment, the rupee was not uniquely

weak — most EM currencies underperformed — but India's

specific exposure to oil imports and the scale of FII outflows

made the pressure more acute than in peer economies.

The RBI intervened repeatedly and visibly, selling dollars

through state-owned banks ahead of market open to prevent

disorderly falls, tightening speculative position limits on

banks' net open foreign exchange exposure, and allowing

forex reserves to fall by approximately $30–31 billion over

the month to fund its market operations. These interventions

were not without effect — they meaningfully reduced

intraday volatility on several occasions, delivered sharp

one-day rupee recoveries after record-low breaches, and

prevented what could have been a more disorderly free fall.

However, they could not alter the fundamental direction of

travel. Each RBI-supported bounce was quickly eroded by

fresh oil-linked dollar demand and FII outflow pressure,

making the central bank's support look more like a series of

controlled pauses than a genuine floor.

The rupee's slide fed back into the broader economy and

markets — worsening the import inflation outlook,

complicating the RBI's room to cut rates aggressively, and

amplifying the Sensex and Nifty corrections through the FII

selling channel. Strategists were broadly aligned in their

assessment: durable rupee stabilisation will require lower

crude prices and a return of foreign inflows — not simply

more intervention, which is already proving costly in terms of

reserve depletion and policy flexibility.

March 2026 delivered one of the most violent crude oil price

shocks in recent memory. Brent crude surged from around

$70–75 per barrel in late February to a peak of $110–117 per

barrel in the third week of the month, before settling just

above $100 per barrel by month end — a monthly gain of

roughly 40–50% that sent tremors through every

oil-importing economy, none more so than India. WTI, the US

benchmark, tracked an almost identical trajectory,

underscoring the purely geopolitical nature of the shock

rather than any region-specific supply quirk.

The proximate cause was the effective closure of the Strait

of Hormuz in early March, triggered by military incidents

directly linked to the escalating US–Israel–Iran conflict in

West Asia. The Strait is the single most critical choke point in

global oil infrastructure, carrying approximately 20% of

the world's oil supply on any given day. Its closure — even

partial or threatened — is the kind of event oil markets

have long feared and never fully priced in during

peacetime. When it materialised, the reaction was

immediate and extreme: Brent jumped roughly 29% in a

single session on 9 March, briefly crossing $100 per

barrel before continuing to climb, as traders scrambled to

price in the prospect of a sustained supply disruption

from Persian Gulf producers that supply the bulk of Asia's

crude imports.

What made the shock particularly difficult to contain was

the near absence of credible shock absorbers. Global oil

markets were already running close to capacity entering

March, with limited spare output available from either

OPEC+ members or non-OPEC producers. Alternative

shipping routes and pipeline options cannot replicate, at

any meaningful speed, the volumes that transit Hormuz

daily. This structural vulnerability meant that even a

partial or temporary disruption generated a price

response far larger than the actual barrels affected —

traders were pricing in duration risk, not just the

immediate shortfall. Algorithmic and momentum-driven

buying in derivatives markets amplified the physical

supply fear, keeping volatility elevated throughout the

month with Brent oscillating between $96 and $110 per

barrel on each fresh geopolitical headline.

OPEC+ attempted a response, but it was too modest to

matter. The group announced a production increase of

approximately 206,000 barrels per day beginning in April

— slightly above market expectations of 137,000 bpd but

representing less than 0.2% of global daily demand. Brent

prices continued rising even after the announcement, as

markets correctly read the move as a confidence signal

rather than a genuine supply solution. The cartel's

influence on near-term price levels was muted; what

drove prices was the duration of Hormuz disruption risk,

not quota arithmetic.

For India, the impact was acute and multi-dimensional. In

rupee terms, crude surged from approximately ₹5,700 per

barrel at end-February to over ₹9,000–9,500 per barrel

intra-month, before moderating to around ₹9,200–9,300

by month end. This translated directly into a widening

import bill, rupee depreciation pressure, bond yield rises,

and the equity market sell-off that defined Indian

financial markets through March — making crude oil the

single most consequential external variable of the

month.

March 2026 will be remembered as the month Indian

mutual funds stepped up as the market's most

consequential domestic stabiliser. As Foreign Portfolio

Investors pulled out a record ₹1.23 trillion from Indian

equities — the largest monthly FPI outflow ever recorded

— domestic mutual funds deployed an estimated ₹1.05

trillion into the market, absorbing the bulk of that external

selling and preventing what could have been a far more

catastrophic correction. Analysts broadly agree that

without this domestic buying cushion, the Nifty's 11%

monthly decline — already the steepest since March 2020

— could have deepened to 15–18%.

The buying was deliberate and concentrated. Fund

managers reduced cash holdings and scaled into

large-cap and index-linked schemes during the worst

sell-off days, particularly when crude oil crossed $110

per barrel and war headlines intensified. This demand

flowed directly into the Sensex and Nifty heavyweights —

banks, energy, infrastructure, and large-cap IT — helping

narrow intraday losses and underpin visible recoveries

in the final 7–10 trading sessions of the month. The SIP

engine remained a key enabler: with equity-oriented

schemes having received net inflows of over ₹25,000

crore in February, AMCs had fresh capital to deploy into

discounted equities without disrupting their flow

pipelines.

Not all segments fared equally well. Debt fund inflows

fell sharply, with investors rotating into liquid and

short-duration products for safety. Gold ETF inflows

collapsed by 78%, as investors gravitated toward

physical bullion. Passive scheme inflows also weakened

meaningfully. On the equity side, all mutual fund

categories ended the calendar year to date in negative

territory, with some focused and ELSS schemes down

12–16% — a painful reminder of concentration risk in

volatile markets. NFO activity, however, remained brisk,

with several new launches across equity, debt, and

arbitrage categories reflecting the industry's longer-term

confidence despite the near-term turbulence.