Topic 1: EQUITY: WAR STRUCK

March 2026 was a month, Indian equity investors would

rather forget. Both the Sensex and Nifty 50 ended deep in

the red, battered by a toxic cocktail of geopolitical shock,

surging crude oil prices, and relentless foreign selling.

What began as a volatile but seemingly manageable

correction quickly snowballed into one of the most

punishing months for Indian benchmarks in recent

memory, erasing months of gains and wiping out an

estimated ₹48 lakh crore of investor wealth in a matter of

weeks.

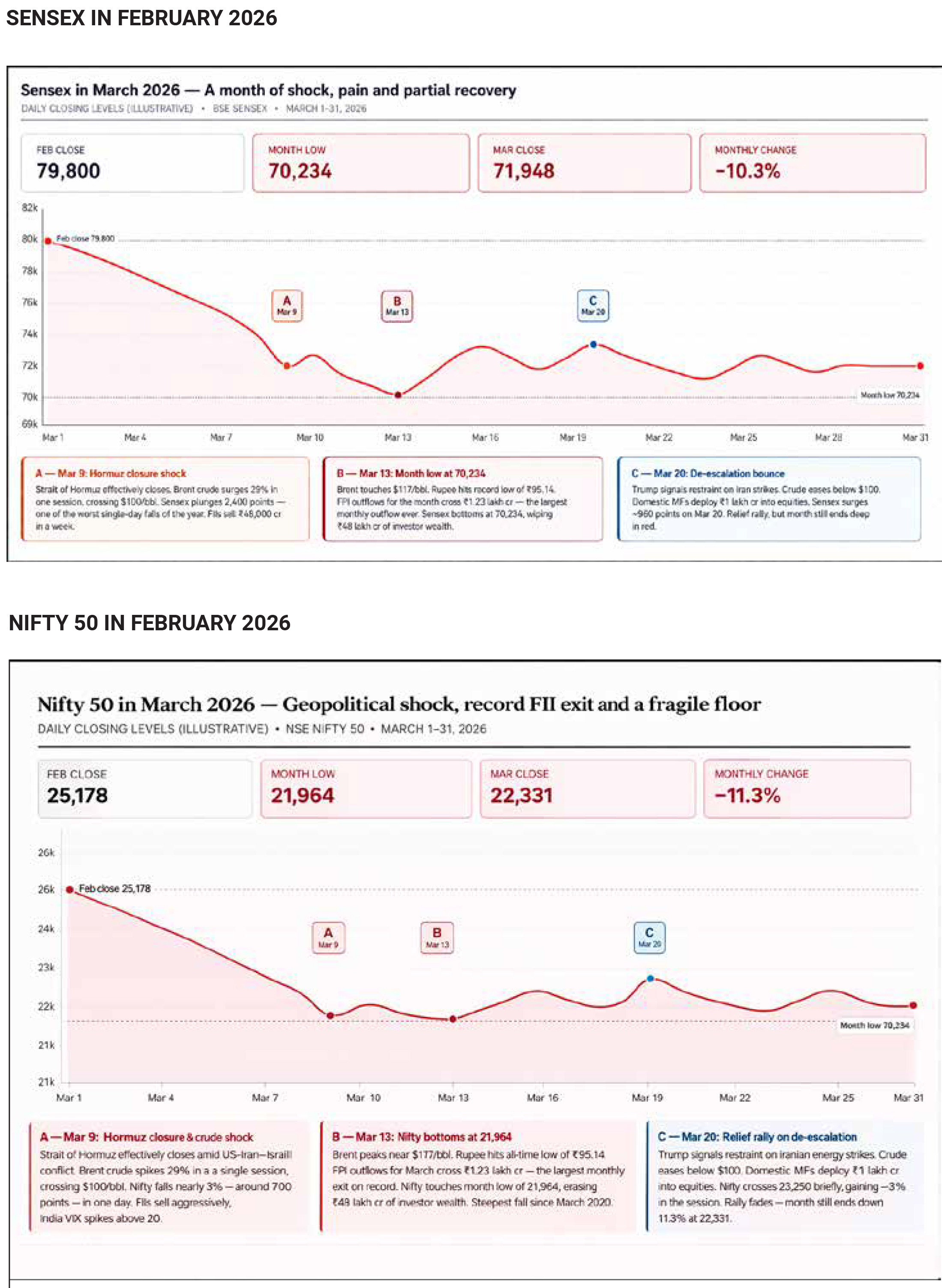

The Nifty 50 closed March at approximately 22,331 — a

fall of roughly 2.9% from its February end level of around

25,178. The Sensex fared even worse, shedding over 10%

across the month to close near 71,948, down sharply

from its late-February levels. March was punctuated by

repeated gap-down opens, savage intraday swings, and

brief but ultimately hollow relief rallies that lured buyers

in, only to reverse and fade. The India VIX, the market's

fear gauge, spiked above 20 for extended periods — a

clear signal that institutional players were paying heavily

for downside protection, and that genuine confidence

had left the room.

The cause of March's mayhem was a sharp escalation of

geopolitical tensions in West Asia. Conflict involving

Iran-linked flashpoints — which had been simmering

through February — intensified dramatically around the

last few days of that month, triggering a classic risk-off

cascade across global markets. For India, the damage

was immediate and multi-channelled. The most direct hit

came through crude oil. Brent crude surged above $100

per barrel in the first two weeks of March — a

psychologically significant threshold that set alarm bells

ringing for India, the world's third-largest oil importer.

Every dollar increase in crude adds meaningfully to

India's import bill, widens the current account deficit,

pressures the rupee, and stokes inflation. Markets

moved quickly to price in all these consequences. The

Nifty fell nearly 3% in a single session on 9 March, with

the Sensex shedding over 2,400 points in one of the

sharpest single-day drops in recent months.

If geopolitics lit the fire, Foreign Institutional Investor

selling poured fuel on it. FIIs turned aggressive net

sellers in March, with net outflows estimated at

₹14,000–₹48,000 crore over the course of the conflict's

escalation. The logic was straightforward: when

geopolitical risk spikes, global funds rotate out of

emerging market equities — perceived as higher-risk

assets — and into safe havens like US treasuries, gold,

and the dollar. India, despite its relatively strong

domestic macroeconomic fundamentals, was caught

squarely in this global de-risking wave.

The rupee came under simultaneous pressure, sliding to

fresh lows against the dollar. A weaker rupee

compounds the crude oil pain further — India pays for its

oil imports in dollars, so every rupee of depreciation

makes an already expensive barrel of oil even costlier in

local currency terms. This feedback loop between crude,

the rupee, and inflation fears kept sentiment firmly

negative throughout most of the month.

The pain was not evenly distributed across the market. The sectors that bore the heaviest losses were those most exposed to the dual threat of higher crude and tighter financial conditions — banks and NBFCs, automobile companies, aviation stocks, paint manufacturers, and logistics firms. These sectors together carry significant weight in both the Sensex and Nifty, which amplified the benchmark-level damage. There were pockets of resilience. Upstream oil and gas producers benefited from higher crude realizations and select IT and pharmaceutical names attracted some safe-haven interest on the back of rupee depreciation, which boosts export earnings. However, these sectors are relatively underweight in the large-cap indices compared to financials and consumer-facing businesses, so their gains were insufficient to offset the broader carnage. Interestingly, mid-cap and small-cap indices showed slightly better relative performance during parts of the month — but even these couldn't escape the overall negative tide. The month wasn't entirely without hope. In the latter half of March, comments from US President Donald Trump hinting at a more restrained approach toward Iranian energy infrastructure — effectively signalling a pause in the threat of direct military strikes — triggered sharp short-covering rallies. On 20 March, the Sensex surged nearly 960 points and the Nifty briefly crossed 23,250 as crude eased and risk appetite ticked up globally. Global equity funds recorded their largest weekly inflow in over two and a half months in the week ending 25 March, as markets reacted positively to the de-escalation signals. FII outflows from India slowed noticeably in this window, and some short covering in index heavyweights provided temporary support. But the key word is temporary. Each time Trump's tone softened, markets rallied. Each time his rhetoric hardened again — as it did in early April with fresh threats — the selling pressure returned. The de-escalation comments acted more as a brake on panic than as a genuine catalyst for a structural reversal. By month end, FII flows remained in net negative territory. March 2026 has been a sobering reminder of how quickly external shocks can overwhelm strong domestic fundamentals. India's GST collections, formal sector activity, and credit growth all remained reasonably healthy through the month — but these factors were simply no match for the combination of a $100 crude shock, record FII outflows, and a global flight to safety.