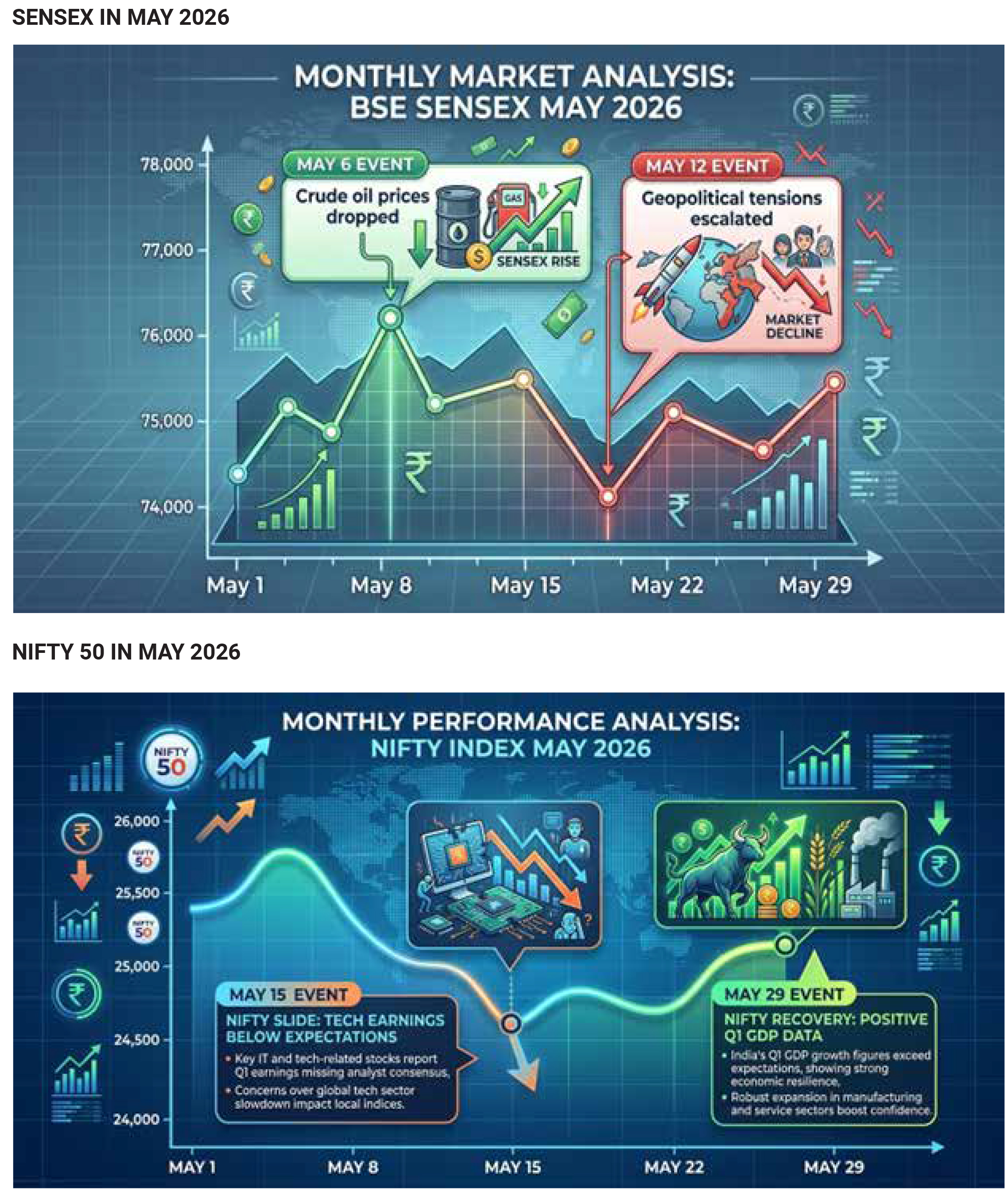

May 2026 proved to be a challenging month for Indian equity markets as the benchmark Sensex and Nifty indices ended in negative territory after a strong rally in April. The BSE Sensex declined approximately 2.8% during the month, while the NSE Nifty 50 lost nearly 1.9%, reflecting a period of consolidation and correction rather than a full-fledged market downturn. The month began with signs of resilience, as investors initially remained optimistic following April’s impressive gains. However, as May progressed, a combination of global and domestic headwinds gradually eroded market sentiment. On 5 May, the Sensex closed at 77,017.79 while the Nifty settled at 24,032.80 after a weak trading session. A day later, both indices staged a sharp recovery, with the Sensex surging over 940 points to 77,958.52 and the Nifty gaining nearly 300 points to close above 24,330, supported by a sharp decline in crude oil prices and optimism surrounding possible diplomatic progress between the United States and Iran. This rally provided temporary relief and boosted confidence in sectors such as banking, financial services, real estate, automobiles, and aviation, all of which tend to benefit from lower energy costs and improving economic sentiment. Nevertheless, these gains proved difficult to sustain as fresh geopolitical uncertainties macroeconomic concerns resurfaced. emerged and Sectoral performance during May reflected the uneven nature of market sentiment. Financial services and banking stocks emerged as relative outperformers during periods of strength. Several factors contributed to the resilience of financial stocks, including expectations of continued credit growth, improving asset quality, strong earnings performance, and supportive economic conditions. Public sector banks also benefited from ongoing government reforms and improved balance-sheet health. Lower crude oil prices during the early part of the month further boosted confidence in rate-sensitive sectors, including banks, real estate, and automobiles. Telecom stocks also performed well during strong market sessions, supported by stable earnings expectations and defensive characteristics. Mid-cap stocks demonstrated greater resilience than large-cap indices during the month. The Midcap Nifty managed to outperform benchmark indices despite overall market weakness, indicating that investor interest in select growth-oriented companies remained intact. Broader themes such as defence, infrastructure, real estate, and select industrial sectors continued to attract attention from investors seeking long-term growth opportunities. Defence-related stocks, in particular, benefited from strong order books and government emphasis on domestic manufacturing and self-reliance initiatives. In contrast, energy, FMCG, utilities, and capital market-related sectors faced considerable pressure. Energy companies struggled amid concerns regarding higher input costs and volatile crude oil movements. Major stocks such as ONGC, Reliance Industries, and

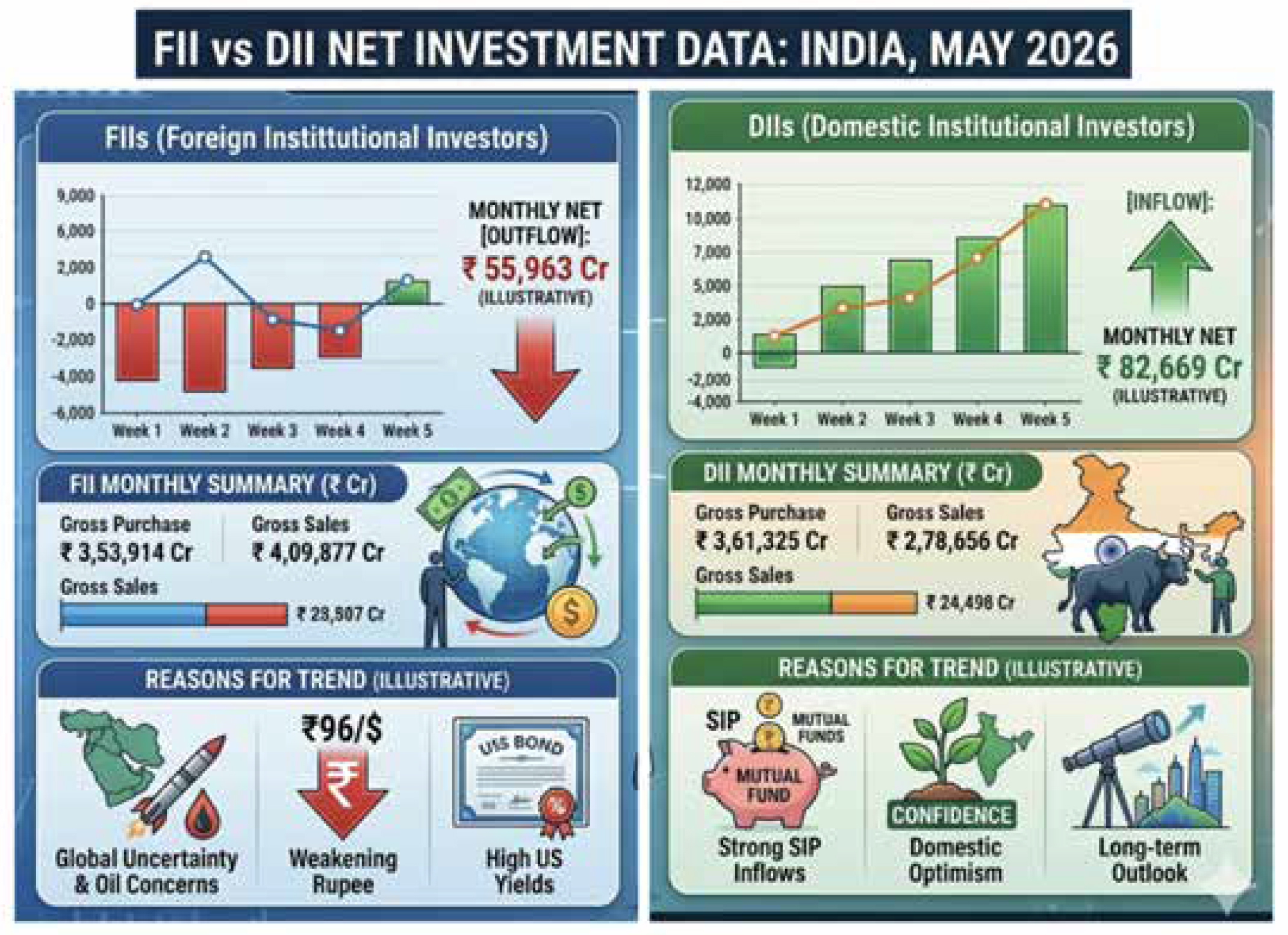

Power Grid were among the notable laggards during certain trading sessions. FMCG companies faced challenges arising from inflation concerns and rising raw-material costs, while utility stocks suffered from broader risk-off sentiment. As the month progressed, even some previously strong sectors such as defence and banking experienced profit-taking, contributing to the overall market decline. The most significant factor weighing on Indian equities during May was the sharp rise in global crude oil prices. Brent crude remained elevated throughout much of the month and at times crossed the critical US$100 per barrel level, raising concerns about imported inflation and the potential impact on India’s current account deficit. As India imports the majority of its crude oil requirements, higher energy prices directly affect inflation expectations, corporate profitability, and consumer spending power. Investors feared that sustained high crude prices could lead to increased fuel costs, transportation expenses, and production costs across multiple sectors, thereby squeezing corporate margins and limiting earnings growth. These concerns became more pronounced as geopolitical tensions in West Asia intensified. The deteriorating relationship between Iran and Western powers, combined with concerns surrounding the security of the Strait of Hormuz—a vital global oil transit route—heightened fears of potential supply disruptions. Initially, hopes of a possible US-Iran diplomatic breakthrough supported market sentiment, but as negotiations stalled later in the month, oil prices resumed their upward trajectory, reversing earlier gains in risk appetite and increasing market volatility. Foreign investor activity also played a crucial role in shaping market performance during May. Foreign Portfolio Investors (FPIs) and Foreign Institutional Investors (FIIs) remained persistent sellers of Indian equities throughout the month. Reports indicated that FIIs sold between ₹42,000 crore and ₹56,000 crore worth of shares during May, creating significant pressure on benchmark indices. The outflows were driven by a combination of factors, including elevated crude prices, geopolitical uncertainty, weakening currency conditions, and rising US Treasury yields. Higher yields in the United States increased the attractiveness of dollar-denominated assets, encouraging global investors to shift capital away from emerging markets such as India. Additionally, passive selling linked to MSCI index adjustments contributed to market weakness during key trading sessions. The continued foreign selling reduced liquidity weakened investor confidence, and amplified downward pressure on stock prices, particularly among large-cap stocks that have higher foreign ownership. The depreciation of the Indian rupee further compounded market concerns. During May, the rupee weakened to fresh lows against the US dollar, reflecting both foreign capital outflows and global dollar strength. A weaker rupee increases the cost of imports, especially crude oil, thereby intensifying inflationary pressures. Currency weakness also tends to discourage foreign investment because overseas investors face additional exchange-rate risks when investing in domestic assets. As inflation concerns mounted and expectations of tighter global financial conditions increased, investors became more cautious, leading to reduced risk-taking and increased profit-booking across sectors. The weakening rupee therefore acted both as a symptom and a catalyst of broader market weakness during the month. Despite the challenging environment, domestic institutional investors helped limit the extent of the correction. Domestic mutual funds, insurance companies, and other institutional participants continued to deploy capital into equities, partially offsetting the impact of foreign selling. Their steady buying provided stability during periods of intense volatility and reflected confidence in India's long-term economic growth prospects. Additionally, periodic declines in crude oil prices and occasional improvements in global sentiment triggered short-lived rallies that prevented a deeper market correction. Overall, May 2026 was characterized by heightened volatility, shifting investor sentiment, and a broad-based market correction following April’s strong rally. The decline in the Sensex and Nifty was primarily driven by rising crude oil prices, significant foreign investor outflows, rupee weakness, escalating geopolitical tensions in West Asia, and profit-booking after substantial gains in the previous month. Although there were intermittent rebounds supported by lower oil prices and domestic buying, these positive developments were insufficient to overcome the persistent macroeconomic and geopolitical headwinds. Importantly, the month did not represent a collapse in market fundamentals but rather a healthy consolidation phase in which investors reassessed risks amid changing global conditions. The resilience displayed by financials, mid-cap stocks, and select growth sectors suggests that underlying confidence in the Indian economy remained intact, even as short-term uncertainties weighed on benchmark performance.

In May 2026, the Indian debt market presented a contrasting picture, characterized by resilience at the short end of the yield curve and persistent pressure on longer-duration bonds. While domestic liquidity conditions remained supportive due to proactive measures by the Reserve Bank of India (RBI), a combination of global macroeconomic challenges—including elevated crude oil prices, rupee depreciation, rising US Treasury yields, and foreign investor outflows—prevented a broad-based rally across fixed-income markets. As a result, investors favored short-duration and high-quality debt instruments while remaining cautious toward long-term duration exposure. Government securities (G-Secs) displayed divergent performance depending on maturity. Short-term Treasury Bills and government bonds in the one- to three-year segment emerged as the most stable part of the market. Supported by abundant banking-system liquidity and limited duration risk, these instruments experienced minimal mark-to-market volatility despite broader market uncertainty. In contrast, longer-duration government securities faced considerable pressure. The benchmark 10-year G-Sec yield fluctuated between approximately 6.9% and 7.1% during the month, reflecting investor concerns over inflation, fiscal risks, and global interest-rate trends. Since bond prices move inversely to yields, this increase in yields translated into weaker price performance for long-term sovereign bonds. Duration-heavy gilt funds therefore underperformed compared with short-duration debt funds. Corporate bond markets also witnessed a clear distinction between high-quality and lower-rated issuers. AAA-rated corporate bonds and Public Sector Undertaking (PSU) debt remained relatively resilient throughout the month. Investors continued to view these instruments as safe havens, with yields generally ranging between 7.0% and 7.5% and spreads remaining stable at around 60–90 basis points above comparable government securities. High-quality issuers benefited from strong demand as investors sought dependable accrual income without taking excessive duration risk. However, lower-rated corporate bonds, including AA-rated and below issuers as well as certain Non-Banking Financial Company (NBFC) papers, faced visible selling pressure. Institutional investors became increasingly risk-averse amid global uncertainty, leading to wider credit spreads and reduced appetite for lower-quality debt. In some segments, spreads widened by 100–200 basis points as investors demanded greater compensation for perceived credit risk. Meanwhile, retail-focused gold-loan NBFCs remained active in the primary market, attracting investors through high-yield Non-Convertible Debentures (NCDs) offering coupon rates ranging from 9% to 11.5%. State Development Loans (SDLs) emerged as another favored category among institutional investors. These securities, issued by state governments, offered an attractive balance between safety and yield enhancement. SDLs provided an additional spread of roughly 45–65 basis points over equivalent central government securities while carrying negligible sovereign credit risk. Regular auction schedules and stable demand from insurance companies, pension funds, and mutual funds supported the segment throughout the month. For investors seeking incremental returns without significantly increasing risk, SDLs represented an attractive middle ground between central government bonds and corporate debt. The performance of the debt market during May was shaped by the interaction of supportive domestic liquidity and challenging global macroeconomic conditions. The most significant headwind came from rising crude oil prices. Escalating geopolitical tensions in West Asia pushed Brent crude into the US$90–100 per barrel range, reviving concerns about imported inflation in India. Since the country relies heavily on imported energy, higher oil prices threaten to increase transportation costs, fuel inflation, and worsen the current account deficit. Consequently, inflation expectations remained elevated, with headline consumer inflation projected to stay within the 4.5%–5.5% range. Higher inflation expectations are generally negative for bond markets because investors demand higher yields to compensate for reduced purchasing power, particularly on long-term securities. Currency weakness added another layer of pressure. During May, the Indian rupee depreciated toward ₹95 per US dollar, reflecting both global dollar strength and capital outflows from emerging markets. A weaker rupee not only increased imported inflation but also reduced the attractiveness of Indian debt for foreign investors. At the same time, the US Federal Reserve maintained relatively high policy rates in the 3.5%–3.75% range, making US fixed-income assets more attractive compared with emerging-market debt. This environment encouraged Foreign Portfolio Investors (FPIs) to reduce exposure to Indian bonds. Fiscal-year-to-date foreign selling exceeded US$1.2 billion, contributing to upward pressure on domestic bond yields and particularly affecting longer-duration securities. The RBI’s monetary policy stance also influenced investor behavior. Earlier in 2026, the central bank had reduced the repo rate by a cumulative 50 basis points to support growth. However, the resurgence of inflation risks due to higher crude prices led market participants to believe that the RBI’s easing cycle had effectively ended. Expectations that rates would remain unchanged for an extended period discouraged aggressive duration bets and reduced investor appetite for long-term bonds. Market participants increasingly focused on yield accrual rather than capital gains, favoring short-duration instruments where returns were less dependent on future rate cuts. Despite these challenges, the RBI played a critical role in stabilizing financial conditions and preventing a more severe disruption in debt markets. One of the most significant developments was the approval of a record surplus transfer of approximately ₹2.87 lakh crore (nearly ₹3 trillion) to the Government of India. This historic dividend payout substantially improved government finances, reducing concerns about additional borrowing requirements and easing pressure on sovereign bond supply. The resulting liquidity injection also strengthened banking-system cash balances and supported short-term funding markets. The central bank further supported liquidity through a US$5 billion USD/INR buy-sell swap auction announced in late May. This measure was designed to offset the liquidity drain caused by RBI interventions in the foreign exchange market. As the RBI sold dollars to stabilize the rupee, rupee liquidity was withdrawn from the banking system. Through the swap mechanism, commercial banks provided dollars to the RBI and received rupee liquidity in return, ensuring adequate funding remained available within the financial system. This durable liquidity infusion helped stabilize short-term rates and supported demand for Treasury Bills, commercial paper, and short-duration bonds. Additionally, the RBI implemented regulatory relief by discontinuing the mandatory Investment Fluctuation Reserve (IFR) requirement for banks. This move released capital previously locked in reserve accounts, improving banks’ financial flexibility and enhancing their ability to participate in government and corporate debt markets. Together, these measures created a strong liquidity backstop and prevented a sharper rise in yields despite external pressures. Overall, May 2026 was a month dominated by a rates-and-flows shock rather than a credit crisis. Rising oil prices, rupee weakness, elevated global interest rates, and foreign investor outflows pressured bond prices and pushed yields higher, particularly at the long end of the curve. However, strong RBI liquidity support, structural inflows linked to India's inclusion in global bond indices, and healthy demand for high-quality debt instruments helped stabilize the market. The resulting steep yield curve favored an accrual-oriented investment strategy, with investors concentrating on short-duration government securities, AAA-rated corporate bonds, and State Development Loans. These segments offered attractive risk-adjusted returns while providing insulation from the volatility affecting long-duration bonds. Consequently, the Indian debt market demonstrated resilience despite facing one of the most challenging macroeconomic environments of the year.

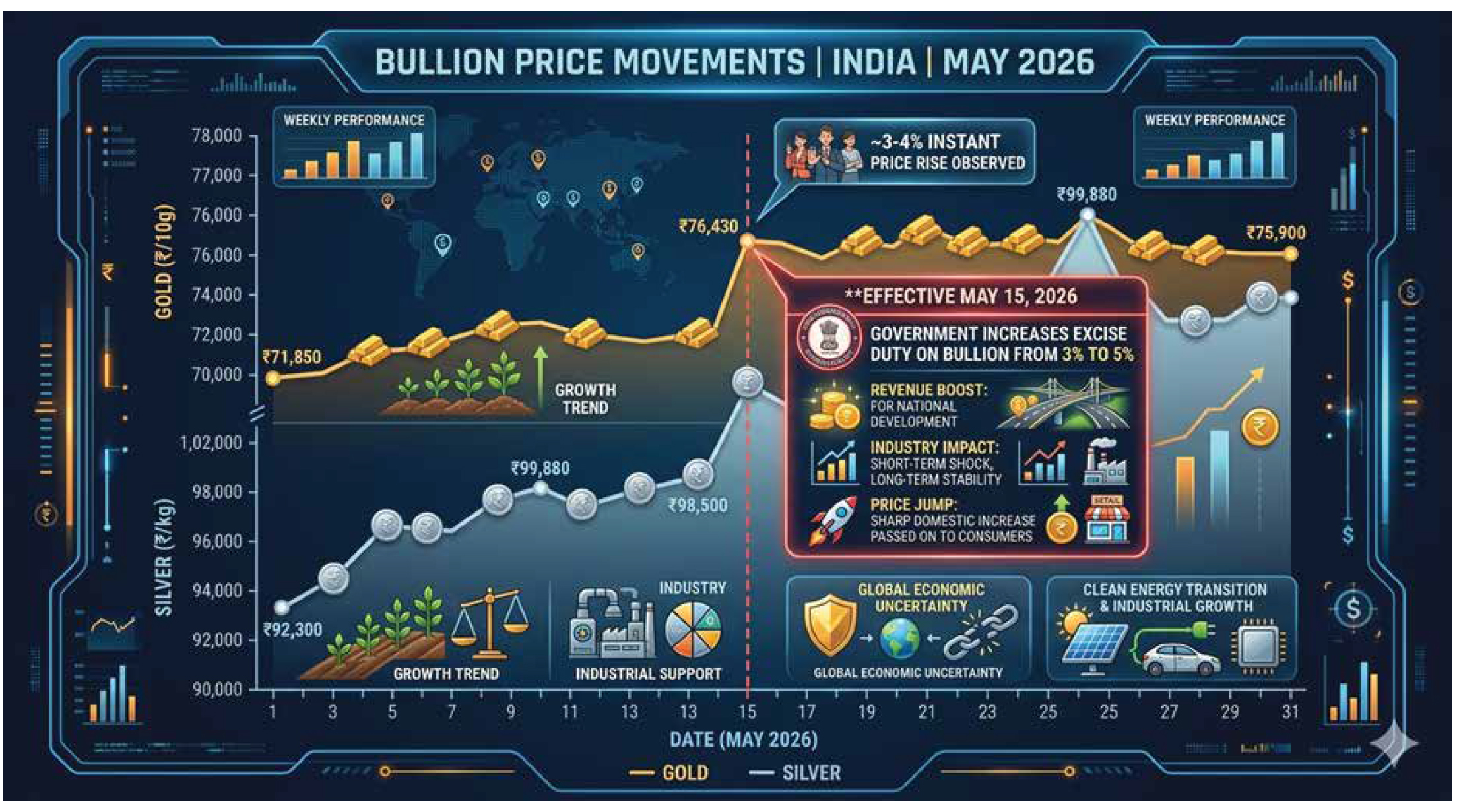

In May 2026, India’s bullion market remained fundamentally strong, although the month was marked by significant volatility due to policy changes and shifting market sentiment. Gold and silver entered the month at historically elevated levels following a strong rally earlier in the year, supported by robust investment demand, global economic uncertainty, inflation concerns, and expectations surrounding interest-rate movements. However, a major turning point occurred on May 13 when the Indian government increased import duties on both gold and silver to 15%. The measure was aimed at reducing bullion imports, narrowing the trade deficit, and supporting the weakening rupee, but it also significantly raised the landed cost of precious metals. The duty hike triggered widespread profit-taking among investors and traders, leading to a temporary correction in domestic markets. By May 14, dealers reported discounts of approximately $200 per ounce compared with official domestic prices, indicating that supply had exceeded immediate demand at the new tax-adjusted price levels. Despite this short-term disruption, bullion prices remained relatively well supported throughout the month. Investment demand continued to be strong as many investors viewed gold and silver as safe-haven assets amid persistent inflationary pressures, geopolitical uncertainty, and volatile financial markets. In contrast, jewellery demand weakened because record-high prices reduced affordability and dampened consumer purchasing, particularly in a challenging economic environment. Global factors also played an important role in shaping price movements. International bullion prices remained elevated due to concerns about inflation, economic growth, and central bank policies, while fluctuations in the US dollar and global interest-rate expectations influenced investor behaviour. Currency movements further affected domestic pricing, as a weaker Indian rupee increased the cost of importing gold and silver, reinforcing upward pressure on local prices. Government policies remained a key determinant of market performance, with the import-duty increase reshaping trade flows and reducing the attractiveness of imports. At the same time, India’s transition away from London’s LBMA precious-metal pricing benchmarks beginning in April 2026 added another layer of change to the pricing environment. During the latter part of the month, gold prices showed moderate gains, including a reported 0.47% rise on May 25, while both gold and silver continued to respond to global market trends, local demand conditions, and exchange-rate movements. Seasonal factors such as festival and wedding-related demand traditionally support gold consumption in India, but elevated prices limited some of this effect during May. Overall, the month demonstrated the resilience of India’s bullion market despite a significant policy shock. While the import-duty increase and subsequent profit-taking capped further gains and created temporary oversupply conditions, the broader outlook for bullion remained positive due to strong investment interest, supportive global macroeconomic conditions, and gold’s enduring role as a hedge against inflation and uncertainty. Consequently, gold and silver continued to perform well in India during May 2026, although the higher tax burden made the domestic market more expensive and was expected to slow imports and moderate demand growth in the following quarter.

In May 2026, the Indian rupee experienced one of its sharpest periods of depreciation in recent years, emerging as one of Asia’s weakest-performing currencies amid a combination of global and domestic economic pressures. At the start of the month, the rupee was trading in the low ₹90s against the U.S. dollar, but persistent selling pressure pushed it steadily lower throughout May. By mid-month, it had breached the psychologically important ₹96-per-dollar level for the first time and touched record lows near ₹96.4–₹96.6, with some market episodes later in the month briefly driving it toward ₹96.9. The currency had lost roughly 1.5% during the month alone and more than 6–7% on a year-to-date basis, reflecting a significant deterioration in investor sentiment and external-sector conditions. The rupee’s decline was driven by a convergence of several adverse factors. The most important was the surge in global crude oil prices, with Brent crude approaching or exceeding $110 per barrel amid geopolitical tensions and disruptions to global energy supply routes. Since India imports more than 85% of its crude oil requirements, higher oil prices substantially increased the country’s import bill and created greater demand for U.S. dollars by oil refiners and importers. This increased demand for dollars put direct downward pressure on the rupee. At the same time, the U.S. dollar remained exceptionally strong globally. Higher U.S. interest rates and elevated Treasury bond yields made dollar-denominated assets more attractive to international investors, encouraging capital to flow toward the United States and away from emerging markets such as India. The widening interest-rate differential between the U.S. and many emerging economies reinforced the dollar’s appeal and contributed to the rupee’s weakness. Global uncertainty also strengthened the dollar’s traditional role as a safe-haven currency. Concerns about geopolitical conflicts, trade disruptions, and slower global growth led investors to seek safety in dollar assets, further boosting demand for the U.S. currency at the expense of emerging-market currencies. Another important factor behind the rupee’s depreciation was persistent foreign capital outflows. Foreign Portfolio Investors (FPIs) continued selling Indian equities and other financial assets during May, reducing demand for the rupee and increasing demand for dollars. These outflows reflected both global risk aversion and the attractiveness of higher-yielding U.S. investments. Simultaneously, India’s balance-of-payments position came under pressure as elevated energy costs widened the trade deficit while capital inflows remained sluggish. The combination of a growing import bill and weaker financial inflows made it increasingly difficult to support the currency through market forces alone. Policymakers responded with a range of measures to contain the depreciation. The Indian government increased gold import duties from 6% to 15% in early May in an effort to curb non-essential imports, conserve foreign exchange reserves, and reduce pressure on the current account deficit. Although this measure affected the bullion market, it was also part of a broader strategy to support the rupee by reducing dollar demand. More importantly, the Reserve Bank of India (RBI) actively intervened in the foreign-exchange market throughout the month. Rather than targeting a fixed exchange rate, the RBI’s objective was to smooth excessive volatility and prevent disorderly market conditions. The RBI also reportedly conducted repeated dollar sales, pre-market interventions, swap operations, and tighter management of banks’ foreign-exchange positions to discourage speculation and stabilize expectations. These actions helped slow the rupee’s decline and enabled a partial recovery below ₹96 per dollar during the latter half of the month. However, the interventions could not completely reverse the depreciation because the underlying drivers—high oil prices, a strong dollar, capital outflows, and trade-balance pressures—remained firmly in place. Despite the challenges, the weaker rupee did provide some benefits. Indian exporters, particularly in the information technology and pharmaceutical sectors, gained competitiveness because their foreign-currency earnings translated into higher rupee revenues. Nevertheless, the broader impact was largely negative, as the weaker currency contributed to imported inflation by increasing the cost of fuel, gold, industrial metals, and other imported goods. Overall, May 2026 was a difficult month for the Indian rupee, characterized by record lows, significant external pressures, and active central-bank intervention. While the RBI successfully prevented a disorderly collapse, the currency remained vulnerable to global market conditions, underscoring the challenges facing India’s external sector in an environment of elevated energy prices, strong U.S. monetary conditions, and persistent capital-flow volatility.

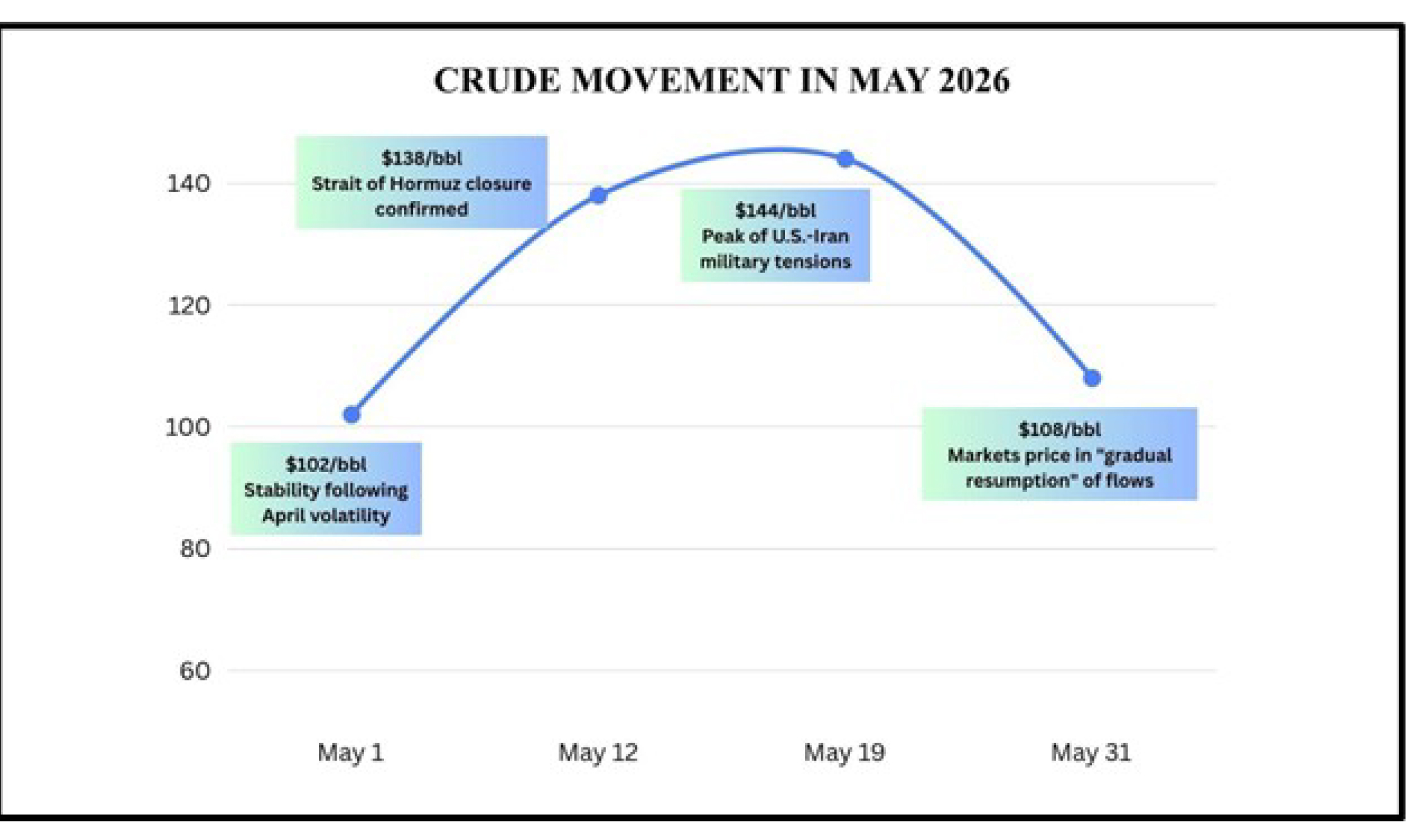

In May 2026, global crude oil markets experienced significant volatility, remaining one of the most important drivers of economic and financial conditions worldwide, particularly for major oil-importing countries such as India. Although oil prices eased somewhat compared with the extreme highs reached in April, they remained elevated throughout the month and continued to place substantial pressure on inflation, trade balances, and currency markets. Brent crude, the global benchmark, began May trading near $100 per barrel before surging sharply during the middle of the month amid escalating geopolitical tensions and fears of major supply disruptions. At the height of market panic, prices briefly approached $140–144 per barrel, levels not seen for many years. However, as concerns over supply shortages moderated and alternative supply routes emerged, prices retreated and eventually stabilized in the range of approximately $106–109 per barrel by month-end. Despite this correction, the average price for May remained high at roughly $108 per barrel, ensuring that energy costs continued to weigh heavily on the global economy. The primary driver of oil-price volatility was the worsening geopolitical situation in West Asia, particularly concerns surrounding the Strait of Hormuz, one of the world’s most strategically important energy transit routes. Roughly one-fifth of global oil shipments pass through this narrow waterway, making any disruption a major threat to international energy supplies. During May, escalating tensions involving Iran, the United States, and regional actors raised fears of prolonged disruptions to shipping routes and oil exports. Markets reacted by incorporating a substantial geopolitical risk premium into oil prices, reflecting the possibility of supply shortages and transportation bottlenecks. At the same time, global oil inventories were already declining, with stocks reportedly falling significantly during April and May. The reduction in inventories weakened the market’s ability to absorb supply shocks, making prices highly sensitive to geopolitical developments and daily news flow. As a result, even rumours of disruptions triggered sharp price movements. barrel Despite these risks, oil prices did not remain above $140 per because the global energy system demonstrated a degree of resilience. Increased production and exports from countries such as the United States, Brazil, and Guyana helped offset some of the supply concerns. Alternative transportation routes and pipeline networks also reduced dependence on the Strait of Hormuz, preventing a complete collapse in global supply. These adjustments eased market fears and contributed to the partial correction in prices later in the month. Nevertheless, oil remained expensive relative to historical averages, and the geopolitical risk premium persisted. For India, the impact of elevated oil prices was amplified by domestic economic conditions. As one of the world’s largest crude-oil importers, India remains highly dependent on foreign energy supplies, importing the majority of its oil requirements. Consequently, high global prices translated directly into a larger import bill and greater demand for U.S. dollars. The situation was made worse by the simultaneous depreciation of the Indian rupee, which weakened to record lows above ₹96 per dollar during May. Because oil is traded internationally in dollars, the weaker rupee meant that Indian refiners and fuel retailers had to pay significantly more in local currency terms, even when global oil prices moderated from their peak levels. This combination of high oil prices and currency weakness created a “double burden” for the Indian economy, increasing costs for businesses and consumers alike. The rise in energy costs also contributed to inflationary pressures across the economy. Fuel prices influenced transportation, manufacturing, and logistics expenses, leading to higher costs for a wide range of goods and services. State-owned oil companies, which had initially absorbed some of the increase in crude prices, gradually began passing these costs on to consumers through higher petrol and diesel prices. As a result, domestic fuel inflation remained elevated despite the modest decline in global oil prices from April’s extreme levels. Policymakers responded with several measures aimed at reducing pressure on the economy and the currency. The government increased gold import duties from 6% to 15% in an effort to reduce non-essential imports, conserve foreign exchange reserves, and help manage the widening trade deficit. India also drew on its Strategic Petroleum Reserves to provide temporary support to refiners, although these reserves were only capable of offering short-term relief. Additionally, policymakers continued promoting long-term initiatives such as ethanol blending and electric-vehicle adoption to reduce dependence on imported oil. Overall, May 2026 demonstrated how geopolitical risks, supply disruptions, and currency depreciation combined to keep crude oil a major macroeconomic challenge for India, even as prices eased somewhat from their most extreme levels.

In May 2026, the Indian mutual fund industry, commanding over ₹70 lakh crore in assets under management (AUM), underwent a major operational overhaul. Fund houses aggressively adapted to the newly enforced SEBI (Mutual Funds) Regulations, 2026,

which introduced sweeping structural changes aimed at increasing transparency and curbing retail mis-selling. A primary focus for Asset Management Companies (AMCs) was transitioning to the Base Expense Ratio (BER) framework. Moving away from a consolidated Total Expense Ratio (TER), AMCs updated their billing architecture to isolate core management fees from external transactional costs like brokerage, STT, and stamp duties. This separation explicitly reveals what investors pay for active fund management versus trading friction. Simultaneously, fund managers spent the month rebalancing portfolios to eliminate product duplication. Under strict new mandates, an AMC's thematic or sectoral equity schemes are now legally barred from sharing more than a 50% portfolio overlap with its other existing equity funds. Marketing strategies also saw a massive shift as SEBI forced the retirement of generic, "goal-based" labels. Traditional marketing gimmicks like "Children's Benefit" or "Retirement Plans" were completely phased out. In their place, the industry pivoted toward Life-Cycle Funds, which utilize scientific, age-based asset allocation that systematically de-risks by scaling down equity exposure over time. To combat intense market volatility, equity managers heavily utilized enhanced macro-buffers. A new regulatory provision allowed them to allocate up to 35% of non-equity assets into gold and silver ETFs, creating vital internal safety nets. Despite this heavy regulatory restructuring, the market remained active. The month closed with a notable surge in targeted New Fund Offers (NFOs), prominently led by passive thematic entries like the Kotak Nifty India Defence Index Fund and the HDFC Nifty Auto Index Fund.