Topic 1: EQUITY: IN FLUX

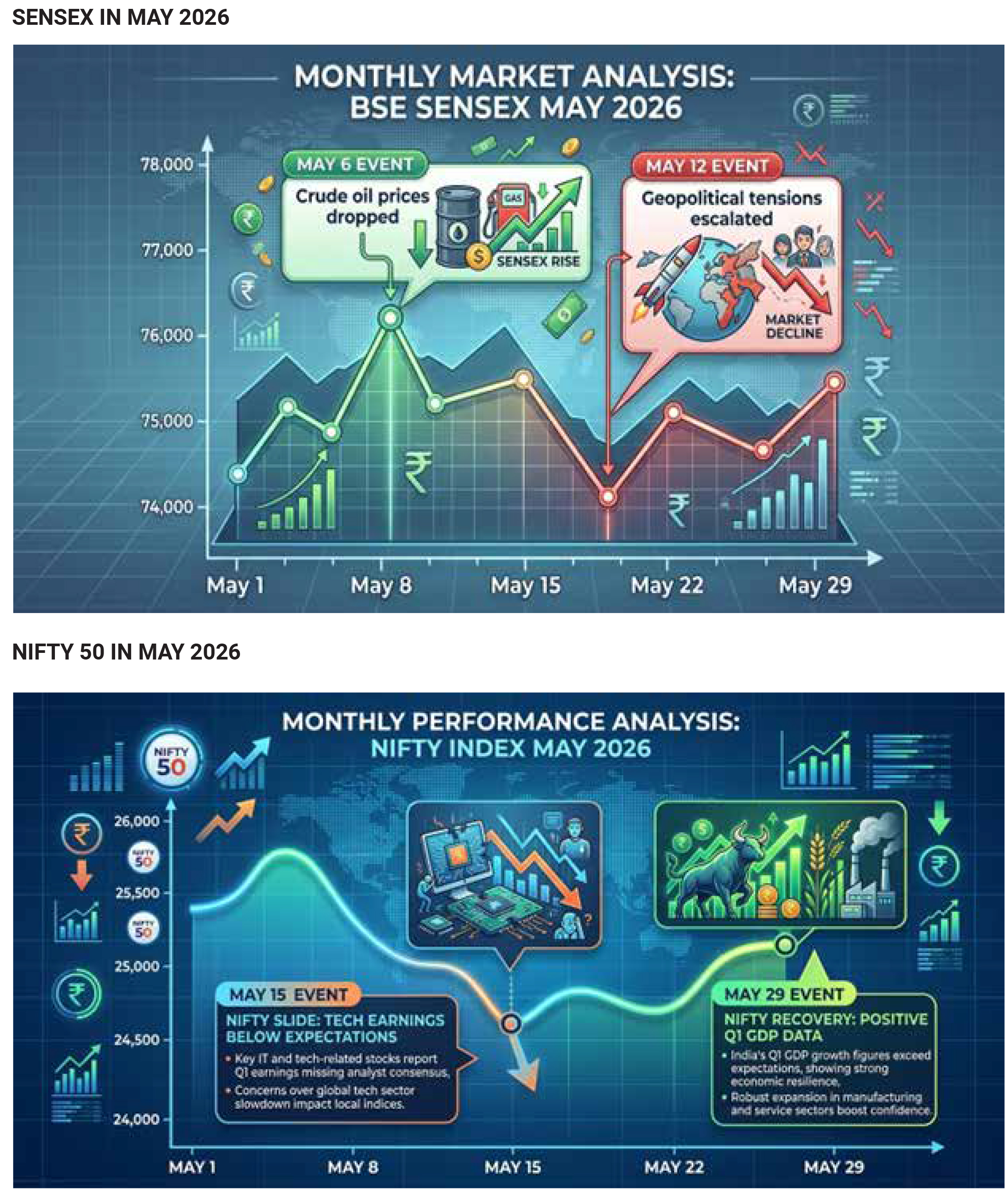

May 2026 proved to be a challenging month for Indian equity markets as the benchmark Sensex and Nifty indices ended in negative territory after a strong rally in April. The BSE Sensex declined approximately 2.8% during the month, while the NSE Nifty 50 lost nearly 1.9%, reflecting a period of consolidation and correction rather than a full-fledged market downturn. The month began with signs of resilience, as investors initially remained optimistic following April’s impressive gains. However, as May progressed, a combination of global and domestic headwinds gradually eroded market sentiment. On 5 May, the Sensex closed at 77,017.79 while the Nifty settled at 24,032.80 after a weak trading session. A day later, both indices staged a sharp recovery, with the Sensex surging over 940 points to 77,958.52 and the Nifty gaining nearly 300 points to close above 24,330, supported by a sharp decline in crude oil prices and optimism surrounding possible diplomatic progress between the United States and Iran. This rally provided temporary relief and boosted confidence in sectors such as banking, financial services, real estate, automobiles, and aviation, all of which tend to benefit from lower energy costs and improving economic sentiment. Nevertheless, these gains proved difficult to sustain as fresh geopolitical uncertainties macroeconomic concerns resurfaced. emerged and Sectoral performance during May reflected the uneven nature of market sentiment. Financial services and banking stocks emerged as relative outperformers during periods of strength. Several factors contributed to the resilience of financial stocks, including expectations of continued credit growth, improving asset quality, strong earnings performance, and supportive economic conditions. Public sector banks also benefited from ongoing government reforms and improved balance-sheet health. Lower crude oil prices during the early part of the month further boosted confidence in rate-sensitive sectors, including banks, real estate, and automobiles. Telecom stocks also performed well during strong market sessions, supported by stable earnings expectations and defensive characteristics. Mid-cap stocks demonstrated greater resilience than large-cap indices during the month. The Midcap Nifty managed to outperform benchmark indices despite overall market weakness, indicating that investor interest in select growth-oriented companies remained intact. Broader themes such as defence, infrastructure, real estate, and select industrial sectors continued to attract attention from investors seeking long-term growth opportunities. Defence-related stocks, in particular, benefited from strong order books and government emphasis on domestic manufacturing and self-reliance initiatives. In contrast, energy, FMCG, utilities, and capital market-related sectors faced considerable pressure. Energy companies struggled amid concerns regarding higher input costs and volatile crude oil movements. Major stocks such as ONGC, Reliance Industries, and

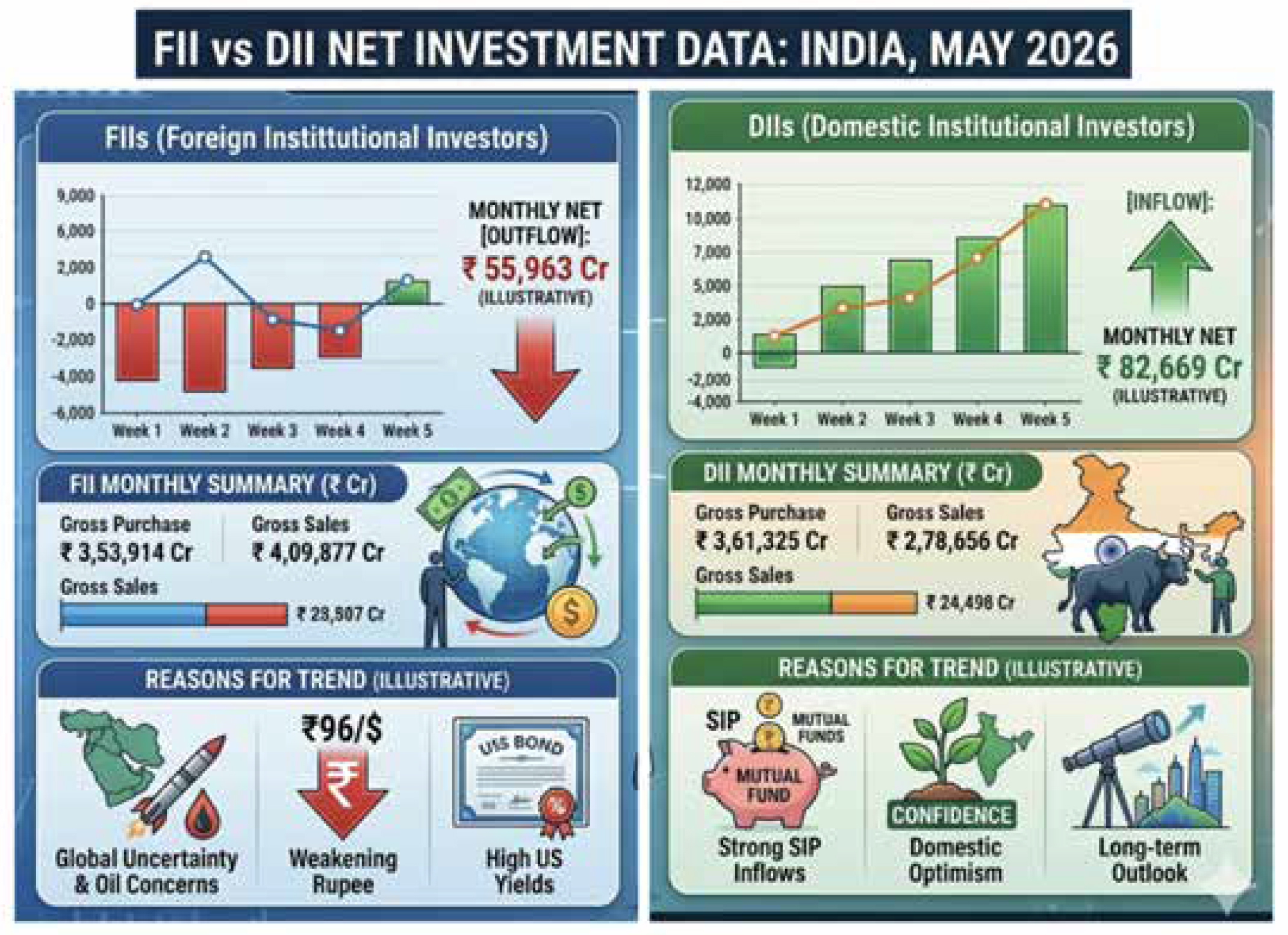

Power Grid were among the notable laggards during certain trading sessions. FMCG companies faced challenges arising from inflation concerns and rising raw-material costs, while utility stocks suffered from broader risk-off sentiment. As the month progressed, even some previously strong sectors such as defence and banking experienced profit-taking, contributing to the overall market decline. The most significant factor weighing on Indian equities during May was the sharp rise in global crude oil prices. Brent crude remained elevated throughout much of the month and at times crossed the critical US$100 per barrel level, raising concerns about imported inflation and the potential impact on India’s current account deficit. As India imports the majority of its crude oil requirements, higher energy prices directly affect inflation expectations, corporate profitability, and consumer spending power. Investors feared that sustained high crude prices could lead to increased fuel costs, transportation expenses, and production costs across multiple sectors, thereby squeezing corporate margins and limiting earnings growth. These concerns became more pronounced as geopolitical tensions in West Asia intensified. The deteriorating relationship between Iran and Western powers, combined with concerns surrounding the security of the Strait of Hormuz—a vital global oil transit route—heightened fears of potential supply disruptions. Initially, hopes of a possible US-Iran diplomatic breakthrough supported market sentiment, but as negotiations stalled later in the month, oil prices resumed their upward trajectory, reversing earlier gains in risk appetite and increasing market volatility. Foreign investor activity also played a crucial role in shaping market performance during May. Foreign Portfolio Investors (FPIs) and Foreign Institutional Investors (FIIs) remained persistent sellers of Indian equities throughout the month. Reports indicated that FIIs sold between ₹42,000 crore and ₹56,000 crore worth of shares during May, creating significant pressure on benchmark indices. The outflows were driven by a combination of factors, including elevated crude prices, geopolitical uncertainty, weakening currency conditions, and rising US Treasury yields. Higher yields in the United States increased the attractiveness of dollar-denominated assets, encouraging global investors to shift capital away from emerging markets such as India. Additionally, passive selling linked to MSCI index adjustments contributed to market weakness during key trading sessions. The continued foreign selling reduced liquidity weakened investor confidence, and amplified downward pressure on stock prices, particularly among large-cap stocks that have higher foreign ownership. The depreciation of the Indian rupee further compounded market concerns. During May, the rupee weakened to fresh lows against the US dollar, reflecting both foreign capital outflows and global dollar strength. A weaker rupee increases the cost of imports, especially crude oil, thereby intensifying inflationary pressures. Currency weakness also tends to discourage foreign investment because overseas investors face additional exchange-rate risks when investing in domestic assets. As inflation concerns mounted and expectations of tighter global financial conditions increased, investors became more cautious, leading to reduced risk-taking and increased profit-booking across sectors. The weakening rupee therefore acted both as a symptom and a catalyst of broader market weakness during the month. Despite the challenging environment, domestic institutional investors helped limit the extent of the correction. Domestic mutual funds, insurance companies, and other institutional participants continued to deploy capital into equities, partially offsetting the impact of foreign selling. Their steady buying provided stability during periods of intense volatility and reflected confidence in India's long-term economic growth prospects. Additionally, periodic declines in crude oil prices and occasional improvements in global sentiment triggered short-lived rallies that prevented a deeper market correction. Overall, May 2026 was characterized by heightened volatility, shifting investor sentiment, and a broad-based market correction following April’s strong rally. The decline in the Sensex and Nifty was primarily driven by rising crude oil prices, significant foreign investor outflows, rupee weakness, escalating geopolitical tensions in West Asia, and profit-booking after substantial gains in the previous month. Although there were intermittent rebounds supported by lower oil prices and domestic buying, these positive developments were insufficient to overcome the persistent macroeconomic and geopolitical headwinds. Importantly, the month did not represent a collapse in market fundamentals but rather a healthy consolidation phase in which investors reassessed risks amid changing global conditions. The resilience displayed by financials, mid-cap stocks, and select growth sectors suggests that underlying confidence in the Indian economy remained intact, even as short-term uncertainties weighed on benchmark performance.