Topic 3: BULLION: DUTY REALIGNED

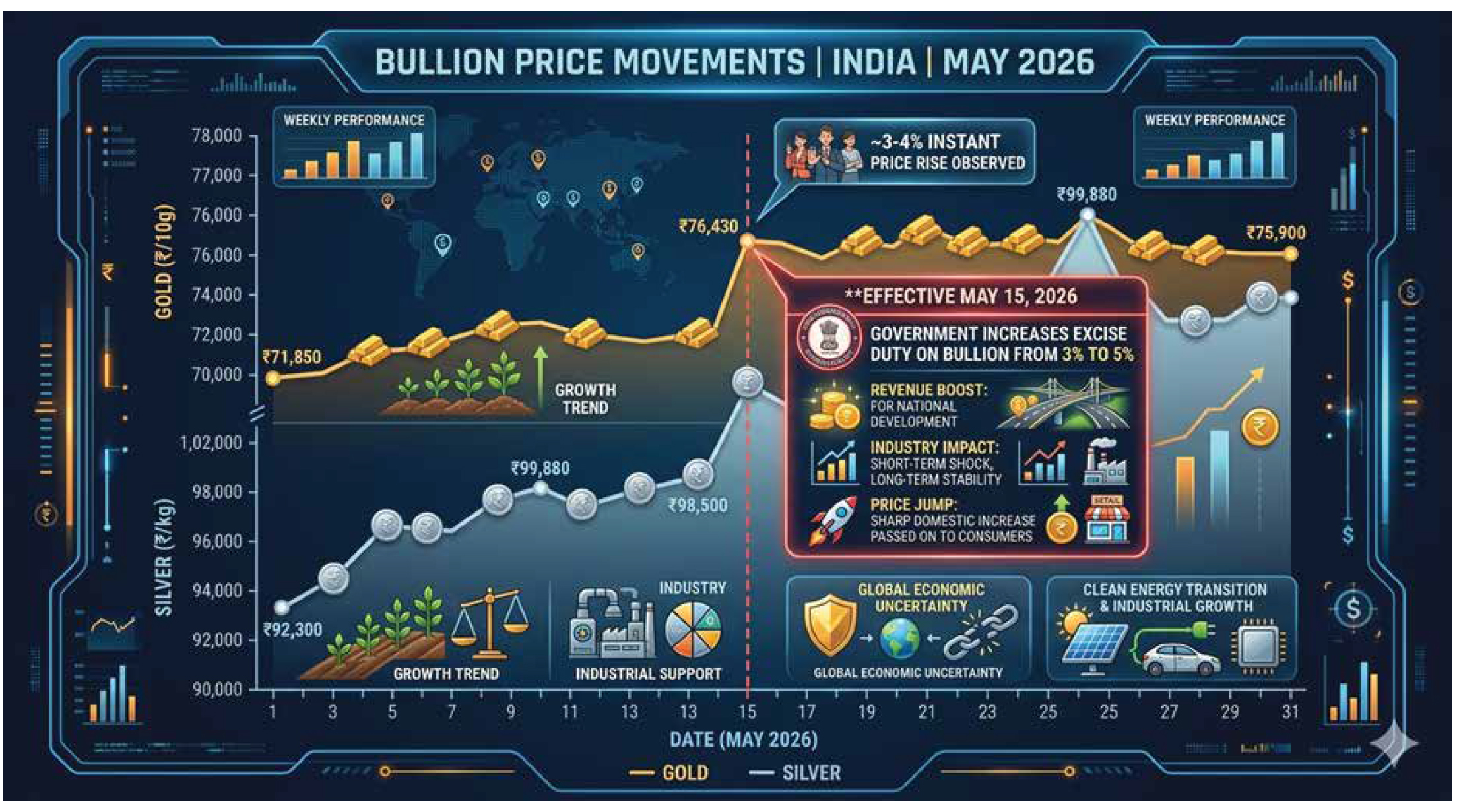

In May 2026, India’s bullion market remained fundamentally strong, although the month was marked by significant volatility due to policy changes and shifting market sentiment. Gold and silver entered the month at historically elevated levels following a strong rally earlier in the year, supported by robust investment demand, global economic uncertainty, inflation concerns, and expectations surrounding interest-rate movements. However, a major turning point occurred on May 13 when the Indian government increased import duties on both gold and silver to 15%. The measure was aimed at reducing bullion imports, narrowing the trade deficit, and supporting the weakening rupee, but it also significantly raised the landed cost of precious metals. The duty hike triggered widespread profit-taking among investors and traders, leading to a temporary correction in domestic markets. By May 14, dealers reported discounts of approximately $200 per ounce compared with official domestic prices, indicating that supply had exceeded immediate demand at the new tax-adjusted price levels. Despite this short-term disruption, bullion prices remained relatively well supported throughout the month. Investment demand continued to be strong as many investors viewed gold and silver as safe-haven assets amid persistent inflationary pressures, geopolitical uncertainty, and volatile financial markets. In contrast, jewellery demand weakened because record-high prices reduced affordability and dampened consumer purchasing, particularly in a challenging economic environment. Global factors also played an important role in shaping price movements. International bullion prices remained elevated due to concerns about inflation, economic growth, and central bank policies, while fluctuations in the US dollar and global interest-rate expectations influenced investor behaviour. Currency movements further affected domestic pricing, as a weaker Indian rupee increased the cost of importing gold and silver, reinforcing upward pressure on local prices. Government policies remained a key determinant of market performance, with the import-duty increase reshaping trade flows and reducing the attractiveness of imports. At the same time, India’s transition away from London’s LBMA precious-metal pricing benchmarks beginning in April 2026 added another layer of change to the pricing environment. During the latter part of the month, gold prices showed moderate gains, including a reported 0.47% rise on May 25, while both gold and silver continued to respond to global market trends, local demand conditions, and exchange-rate movements. Seasonal factors such as festival and wedding-related demand traditionally support gold consumption in India, but elevated prices limited some of this effect during May. Overall, the month demonstrated the resilience of India’s bullion market despite a significant policy shock. While the import-duty increase and subsequent profit-taking capped further gains and created temporary oversupply conditions, the broader outlook for bullion remained positive due to strong investment interest, supportive global macroeconomic conditions, and gold’s enduring role as a hedge against inflation and uncertainty. Consequently, gold and silver continued to perform well in India during May 2026, although the higher tax burden made the domestic market more expensive and was expected to slow imports and moderate demand growth in the following quarter.